Measuring Validity for Moving Average Forecasts

| Introduction.

Again we are going to work at developing

more objective measures for the quality of a forecast. We are again

going to focus on APE = Average Percentage Error.

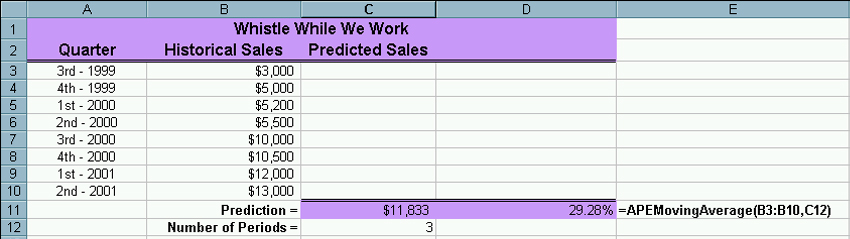

Due to some previous familiarity I will start by showing the spreadsheet

computations for APE for the two-period and three-period moving average

forecasts we did on the Whistle While We Work data.

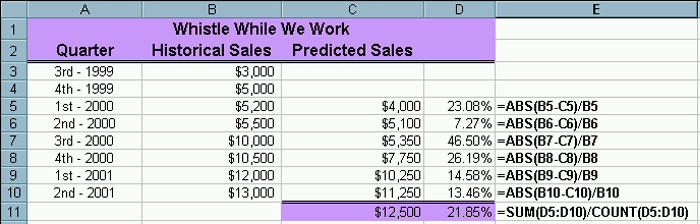

The spreadsheet for the two-period moving average is below. |

| Notice that the average error is about 21.85%, which is

up from many of the error estimates we got for exponential

smoothing. Though none of these approaches is giving a very good

forecast.

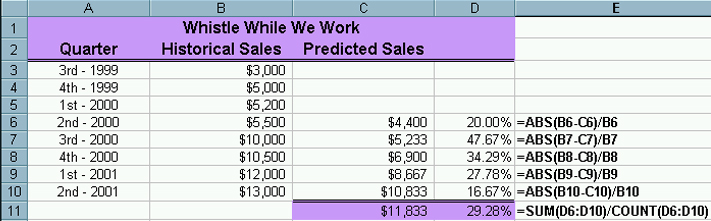

The spreadsheet for the three-period moving average forecast is next. |

| Notice that this error is actually worse than that for

the two-period. This shouldn't be too surprising because the major

thing going on in this data is a trend and we have yet to study any

forecasting methods that work well for trends!

But we need to arrive at some general statements about computing our error terms and computing their averages.

there will be

These all influence the nature of our loops when we compute past predictions and errors. The code for computing the APEMovingAverage function follows. Function APEMovingAverage(Historical, NumberOfPeriods) As Single

' Accumulating the appropriate number of most recent previously observed values

Next PredictionCounter

Next ErrorCounter The code will be discussed in class. You want to check this function on your spreadsheet against other things we've developed. Make sure you choose the number of periods in the moving average the same for both the prediction and the error computation. For the WWWW three period moving average the spreadsheet follows. |